Online shopping and payment are options for everything from ordering groceries to attending educational courses to calling a cab. However, for this convenience, reliable and effective backend operations are needed. Collaboration is required between a number of parties, including buyers, sellers, vendors, logistical partners, and payment processors. And in order to guarantee a business' success, money must be transferred from customers to all of these stakeholders.

Nodal and Escrow are two unique types of bank accounts that were created expressly to manage the challenging money transfers that internet merchants must deal with.

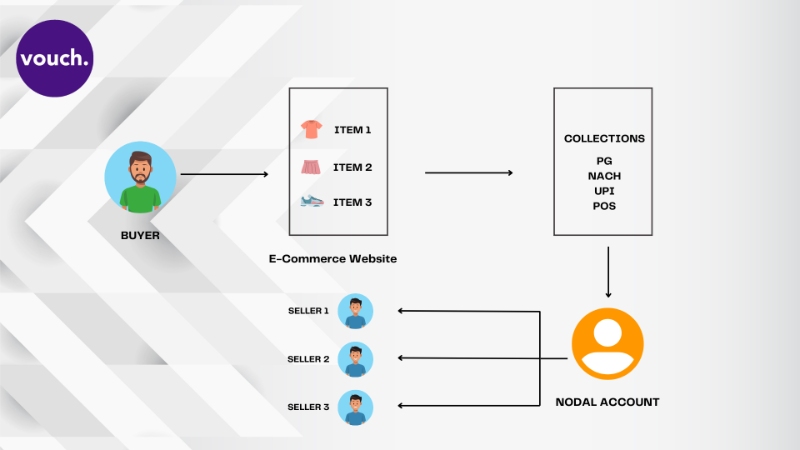

Nodal Accounts

Nodal accounts, also known as nodal banks, are unique internal bank accounts required by the RBI for companies that act as middlemen between buyers and sellers.

So what does an intermediary actually do? So, in such case, your internet business would act as an intermediary:

For the benefit of your vendors, you collect money from customers online. Where you are merely sourcing the goods and not making them yourself. Where you partially or not at all pay for the goods you purchase or stock.

The multi-layered interactions between numerous unidentified parties—customers, vendors, payment gateways, etc.—are what make online commerce so stunning. The trust between these parties will erode if payments are not made on schedule.

A nodal account is used to account for the "trust" element. Customers' and vendors' interests are protected, ensuring that payments are collected, processed, and paid out to the appropriate vendors without unnecessary delay.

Below is an illustration of a nodal account's transaction flow at a marketplace:

The nodal account essentially serves as a temporary safe to hold and disperse the funds to appropriate parties.

Payouts are not just for sellers and vendors. However, they also contain additional entities like transportation costs for logistics partners, fees for middlemen, and commissions for payment processors.

Escrow Accounts

Before the advent of the internet, have you ever heard the term "Escrow"?

Escrow is thought to have been utilized as far back as the Middle Ages. Escroe was the term for a tiny scrap of paper, parchment, or other material that served as a deposit of trust or security and was held by outside parties until a later condition was met.

The main goal of an escrow account is still to establish confidence and security in online transactions. A temporary vault of funds maintained by a dependable third party on behalf of two parties engaged in a transaction and governed by a contract is known as an escrow account. Escrow accounts are typically used in the following situations:

- when a seller and a buyer have never met

- when the agreement is intricate and prolonged

- when the contract's payment and value are substantial.

- where payment is required based on the project's progress toward completion (Eg. a real estate purchase)

Online commerce also makes use of escrow accounts. When the buyer is entirely unknown to the seller, escrow reduces any potential danger. An escrow account is advised, for instance, if you were purchasing used furnishings from an unidentified seller.

The escrow serves as buyer protection and protects you from financial loss due to subpar, damaged, or delayed goods or services. As a result, it lessens the possibility of disputes or chargebacks for the vendor.

This is how an escrow transaction flow would seem

Generally, banks and financial service companies act as escrow agents and charge a fee for escrow services. Before signing up with an escrow agent, make sure to read the terms and conditions thoroughly.

Also, read - Where do you require to have an escrow account?

Digital escrow

Due to their short turnaround times, digital escrow services are proven to be a boon in both domestic and foreign markets. Escrow services have historically been a part of the solution package offered by all banks, with the drawback of a longer setup and processing time. Currently, digital escrow is available, allowing P2P parties to establish accounts and streamlining traditional procedures through online KYCs to enable seamless commercial flows, particularly for online marketplaces.

Digital escrow service in India

Digital escrow services are offered by many companies in India. Among the most trusted is Vouch. Vouch’s Digital Escrow service is a transparent way for buyers and sellers to build trust and secure a clean transfer of product and payment.

Virtual Accounts

Virtual accounts are distinct account numbers that are assigned to traditional, physical bank accounts, also known as settlement accounts. They can be used to send and receive money on behalf of the settlement account, which ultimately holds the funds. Businesses frequently set up multiple virtual accounts, each one dedicated to a different client, transaction, entity, or other business reason.

How do virtual accounts function?

Virtual accounts work in the same way that traditional bank accounts do. They have their own account numbers, help users maintain their balances, and streamline incoming and outgoing transactions. The most notable distinction is that virtual accounts cannot hold money. They receive it, gather the necessary sender information, and forward it to a primary account.

Because of the complexities of the business world, all three - nodal, virtual and escrow accounts have come into play. Each has its own set of rules that are designed to make doing business easier and more transparent.